BRIX

UX research and mobile app design

PROBLEM

There are striking disparities in American households’ wealth. These wealth gaps are even more conspicuous below age 35. Budgeting is essential for reaching financial goals and achieving a measure of security. But having a lower income, less emergency funds, and decreased access to employer-sponsored retirement plans and investment accounts impedes the ability to budget and save effectively.

These challenges led me to wonder:

- How might we engage more low-income Americans under 35 years of age in budgeting so they can feel rewarded and empowered through saving and investing?

RESEARCH METHODS

I got feedback from an advisor helping me to narrow my scope for participants. I didn't know a lot about this demographic. I didn't understand whether or not they were saving and investing, and what challenges they were facing. I needed to find out what budgeting tools were out there. I also needed to find out what these young adults' financial goals were and if/how they planned to achieve them.

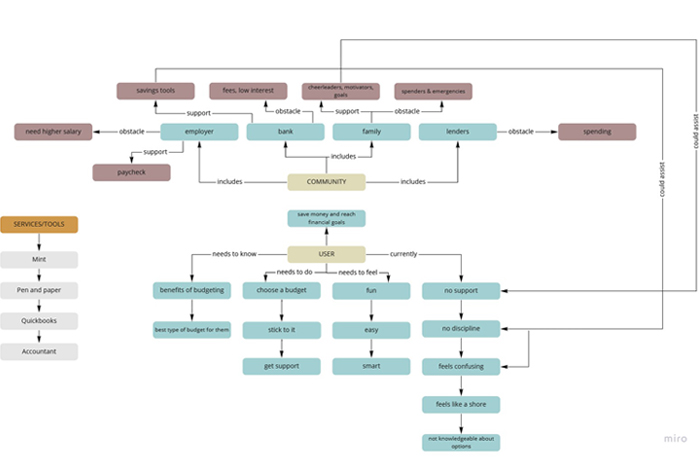

- I created an ecosystem map to understand the available budgeting tools and to identify gaps that existed in assisting people with budgeting.

- I conducted in-depth remote semi-structured interviews with four people in the target audience (Americans below age 35) to learn their feelings toward and experiences with budgeting. I asked questions like:

- Tell me about the last time you implemented a budget.

- How are you currently managing your finances? What apps/tools/software have you tried?

- Is anything/anyone supporting you in your efforts to budget?

- What is your biggest challenge to saving money?

- How might budgeting change your life?

- I conducted remote user tests with four participants to gain general first impressions and to gain feedback on their understanding of my initial lo-fidelity product prototype. I wanted to understand:

- Can people understand the purpose of the app?

- Do they understand how to enter their financial information?

- Do they understand how to continue to engage with the app after logging out?

INSIGHTS

Analysis was done by isolating key themes from participants' interviews. I also plotted feedback insights onto axes to assist in understanding which problems should be addressed in subsequent iterations.

- Budgeting is very personal; there is no one-size fits all approach

- Budgeting takes time to learn

- Major challenges: controlling spending, emergency spending, having a low income

- Ecosystem map revealed need for support, i.e.: motivators, cheerleaders, goals, just-in-time education

PROTOTYPING

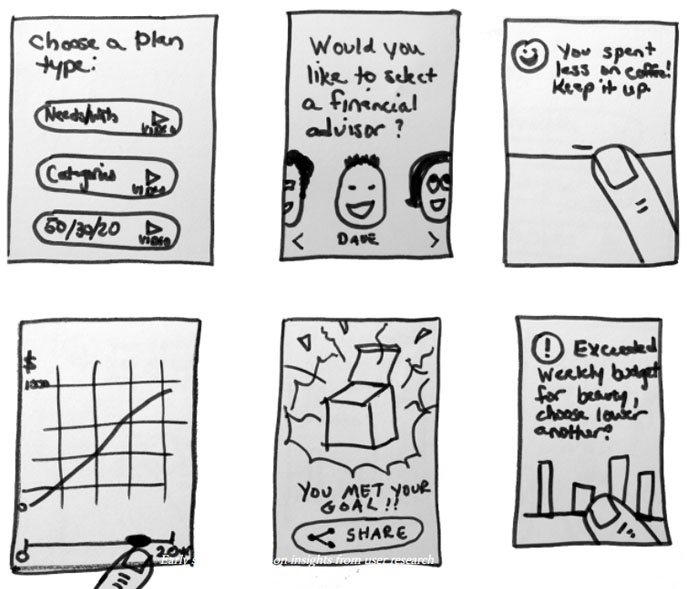

These insights were surprising and led me to braistorm many ideas I hadn't anticipated, such as incorporating social media in the budgeting tool. Based on my insights gained, I developed the following requirements for my prototype:

- Connect users with friends and family for support

- Show users how small changes can add up over time

- Allow users to choose and customize their budget

- Offering optional instructional videos

- Encouraging notifications and rewards

- Visual graphing function

- Personalized goals

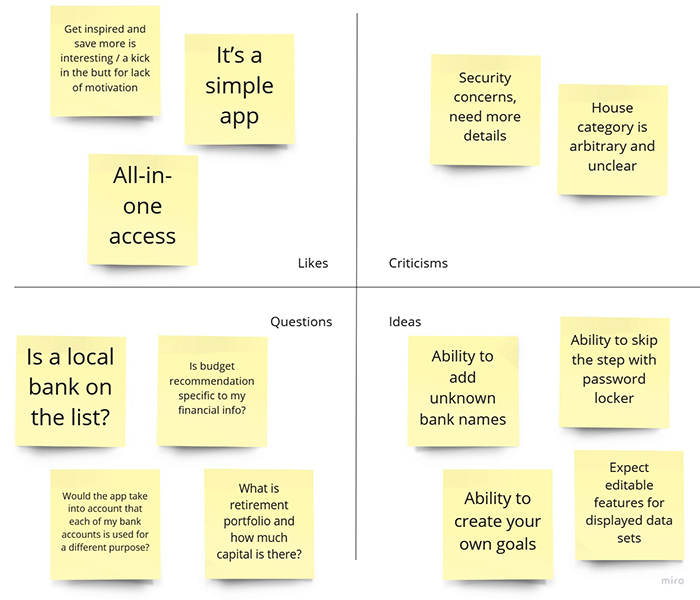

I tested 4 low-income Americans under 35 years of age. Participants were encouraged to think aloud and describe the purpose of each screen. The task was: “You are trying to save or invest to meet a long-term goal. You will sign up for a personal budgeting tool for help.” After the test, they answered questions about the budgeting tool and their impressions.

- The main takeaway was concern about security: how their data was being stored and used

- Their major concern was customization, users wanted: custom budget categories, custom bank names, custom goals

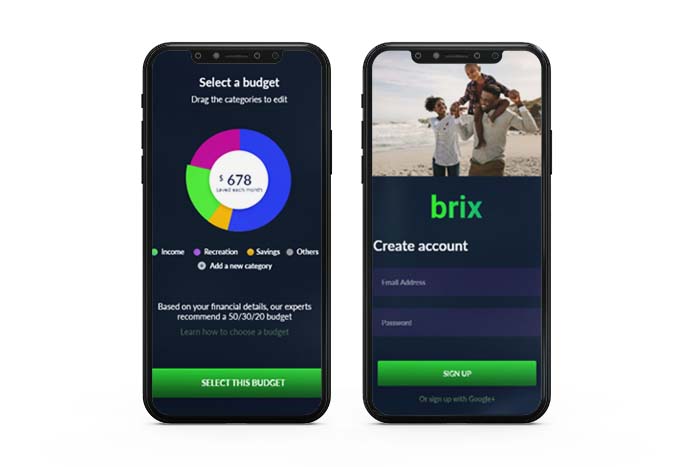

For the mid-fidelity prototype, user requested greater breadth and depth, as well as greater interaction and visual fidelity. I also addressed security by adding more layers of privacy and detailed information. I addressed customization concerns by adding custom options and editable goals.

REFLECTIONS

My research findings led me in a completely new direction -- using social aspects to increase user participation in budgeting. Moving forward, I would incorporate more gamification elements to incentivize use of the app through fun and competition, while doing more user testing within the target age group. I am interested to see how these users would respond to in-app investment opportunities which are not provided through employers.

HOSPITAL APP

Formative research for hospital patient mobile app

MAP THE MONEY MAZE

Research and design for educational mobile app

KIDS IN TECH

Research and website redesign to increase engagement